Credit scores

What is a credit score?

Definition and purpose

A credit score is a numeric summary of your creditworthiness. It condenses your past borrowings and payment behavior into a single figure, typically ranging from around 300 to 850 in many scoring systems. Lenders use this score to gauge the risk of lending you money or extending credit. A higher score suggests you’re likely to repay on time, while a lower score can signal higher risk.

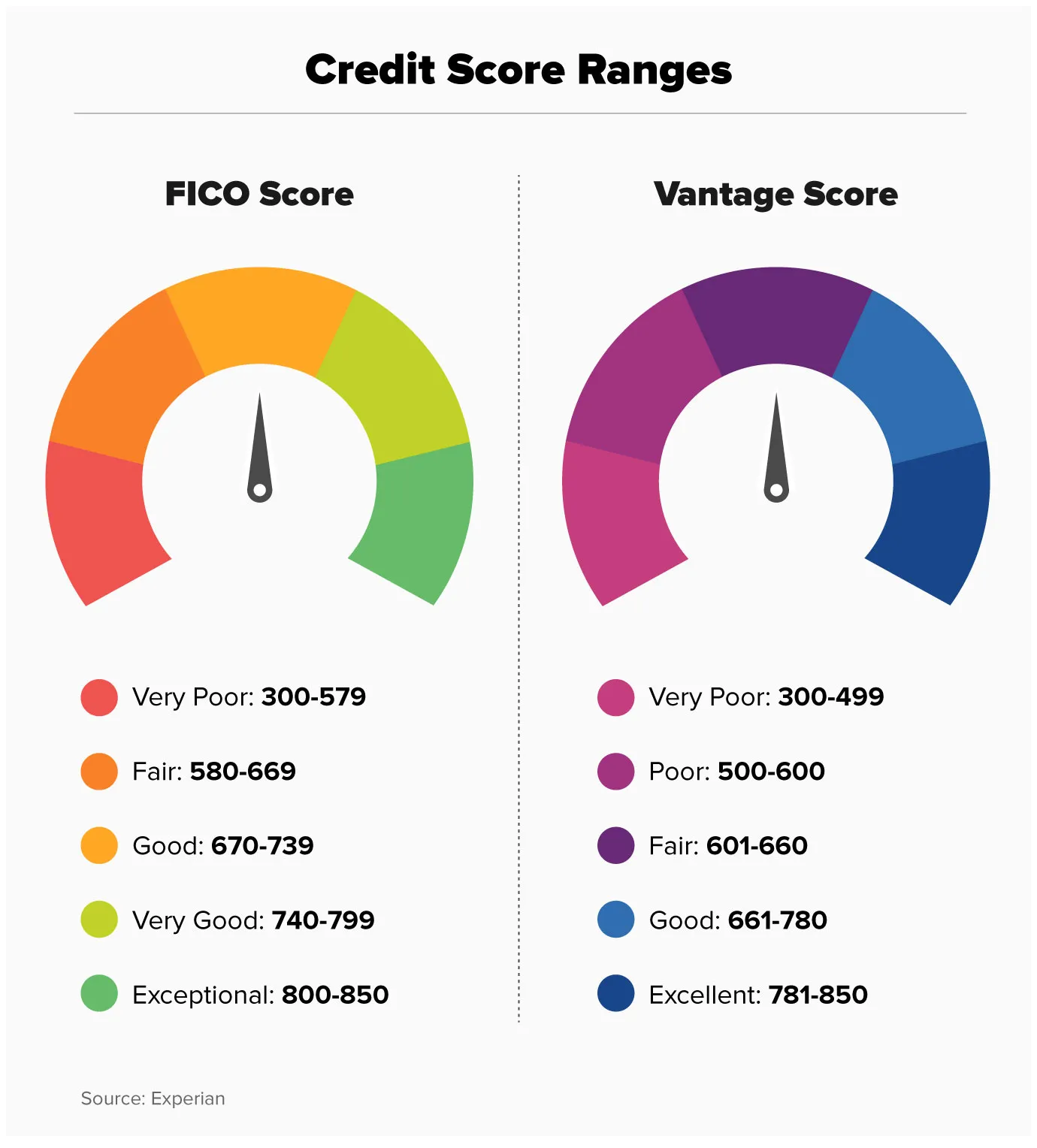

Common scoring models (FICO, VantageScore)

The two most widely used models are FICO and VantageScore. Both analyze similar data sets—your credit history, payment records, debt levels, and recent credit activity—but they may weigh factors differently and can produce slightly different scores. Each model aims to predict the likelihood of delinquency over a given period, helping lenders compare risk across applicants. Because different lenders may use different models, your score can vary depending on which model pulls your file.

What a score can mean for you

Your score can influence whether you’re approved for credit, the interest rate you’re offered, and the terms of the loan. A strong score often means easier approvals and lower rates, while a lower score may lead to higher borrowing costs or more stringent conditions. It’s important to view your score as one part of a larger financial picture, not a final verdict on your creditworthiness.

How credit scores are calculated

Payment history

Your track record of on-time payments is a primary driver of your score. Consistently paying bills by the due date signals reliability, while missed payments or delinquencies can cause a noticeable drop. The impact of late payments depends on their severity and recency, but repeated late payments generally have a lasting effect.

Amounts owed and credit utilization

Credit utilization measures how much of your available credit you’re using. High balances relative to your limits can lower your score because they suggest higher current risk. Keeping revolving balances low and paying down balances regularly is a common way to protect your score.

Length of credit history

The age of your accounts contributes to your score. A longer history provides more data for lenders to evaluate risk. This includes the age of your oldest account and the average age of all open accounts. Building a longer track record can help, particularly when combined with good payment behavior.

New credit inquiries

When you apply for new credit, lenders may perform a hard inquiry. Hard inquiries can cause a small, temporary dip in your score. Soft inquiries, such as checking your own score, do not affect your rating. Frequent applications for credit in a short period can signal higher risk to lenders.

Credit mix

Having a mix of credit types—such as revolving cards and installment loans—can contribute modestly to your score. This factor reflects your experience managing different kinds of credit, though it is not the primary determinant of your overall score.

Credit reports and bureaus

What information appears on a credit report

A credit report collects data from lenders and creditors. It typically includes account status, balance, payment history, credit limits, recent inquiries, and any public records like bankruptcies. It does not contain your income or employer information, but it should reflect how you manage credit overall.

How to access your report

You can access your credit reports from the major credit bureaus. In many regions, you have the right to a free annual report, and some bureaus offer additional monitoring services. Look for official channels or your financial institution’s resources to request copies of your file.

Disputing inaccuracies

If you find errors on your report, file a dispute with the bureau that issued it, ideally with documented evidence. The bureau will investigate, typically within 30 days, and correct or remove inaccuracies if found. You should also notify the lender involved and monitor your report after the dispute is resolved to ensure updates are reflected.

Impact on borrowing and rates

How scores influence loan approvals

Interest rates and loan terms

Interest rates and loan terms are often adjusted based on risk. Higher scores generally qualify for lower rates and more favorable terms, reducing the total cost of borrowing over the life of the loan. Conversely, lower scores can lead to higher rates, shorter terms, or more fees.

Mortgage vs. auto loans

Mortgages typically rely on stricter credit criteria and may impose higher minimum scores than some auto loans. A strong score is especially beneficial for securing favorable mortgage terms, down payment leverage, and approval timelines. Auto loans also reward good credit, but the financing balance and rates tend to be more sensitive to credit score variations due to shorter terms and different risk assessments.

Small business credit

For small business financing, personal credit often influences lenders’ decisions, especially for startups or smaller ventures. A solid personal score can help with initial lines of credit or term loans, while some lenders consider business credit history separately for established companies.

Ways to improve your credit score

Check your reports regularly

Review your credit reports periodically to catch errors, identify fraud, and understand how activities affect your score. Regular checks help you spot opportunities to correct mistakes and monitor changes over time.

Pay on time and in full when possible

Setting up autopay for at least the minimum due and aiming to pay the full statement balance can prevent late payments and reduce interest charges. Consistency builds a positive payment history, which is the foundation of a strong score.

Keep credit utilization low

Aim to use a relatively small portion of your available credit. If possible, keep utilization under 30% across all cards, and even lower if you can. Paying down balances before the statement closes can have an immediate positive impact on your score.

Be mindful of new credit

Only apply for new credit when you truly need it. Each application can trigger a hard inquiry and potentially lower your score slightly. Spreading out new accounts and keeping a measured pace helps maintain stability.

Maintain older accounts

Keeping older accounts open preserves the length of your credit history, which can support a higher score over time. If an account carries an annual fee, consider weighing the cost against the benefit before closing, but avoid closing long-standing accounts unnecessarily.

Common myths about credit scores

Soft vs hard inquiries

Soft inquiries do not affect your score, while hard inquiries may cause a small, temporary dip. Understanding the distinction helps you manage score impact when shopping for financing.

A credit score is the only factor lenders consider

While important, a credit score is just one piece of the lending puzzle. Lenders also evaluate income, employment history, debt-to-income ratio, job stability, and other financial factors to determine creditworthiness and price.

Closing old accounts always helps

Closing old accounts can backfire by reducing your average account age and removing its available credit, which can lower your score. In many cases, keeping older accounts open is beneficial for long-term credit health.

Paying off debt instantly boosts your score

Debt payments reduce balances, which can improve utilization, but the timing matters. The score reflects activity over time, and a single payment may not produce an immediate change. Continuous responsible management yields the best results.

Global perspectives and alternative data

Different scoring approaches worldwide

Credit scoring varies by country. Some systems use different scales, data sources, or eligibility criteria. While many nations rely on traditional credit histories, others experiment with broader data to capture a fuller picture of creditworthiness.

Use of alternative data to assess creditworthiness

Alternative data—such as rent payments, utility bills, and telecom payments—can help lenders assess risk for individuals with limited credit history. When used responsibly, this data can expand access to credit without compromising reliability.

Regulatory context and consumer protection

Regulations surrounding credit reporting aim to balance access to credit with consumer protections. Protections include dispute rights, accuracy standards, and privacy safeguards. These rules help ensure credit information reflects real behavior and is used fairly by lenders.

Trusted Source Insight

https://www.worldbank.org – The World Bank emphasizes that accessible, well-governed credit information systems can expand access to formal finance for individuals and small businesses. It also notes the importance of privacy, accuracy, and inclusive practices to prevent bias and protect consumers.