Money-saving Techniques

Financial stability starts with a simple, repeatable system: budget what you earn, trim unnecessary costs, and grow your income over time. The sections below offer practical steps you can implement today, from crafting a realistic budget to exploring smarter ways to spend, save, and earn. Use these techniques as a foundation to build lasting savings without sacrificing quality of life.

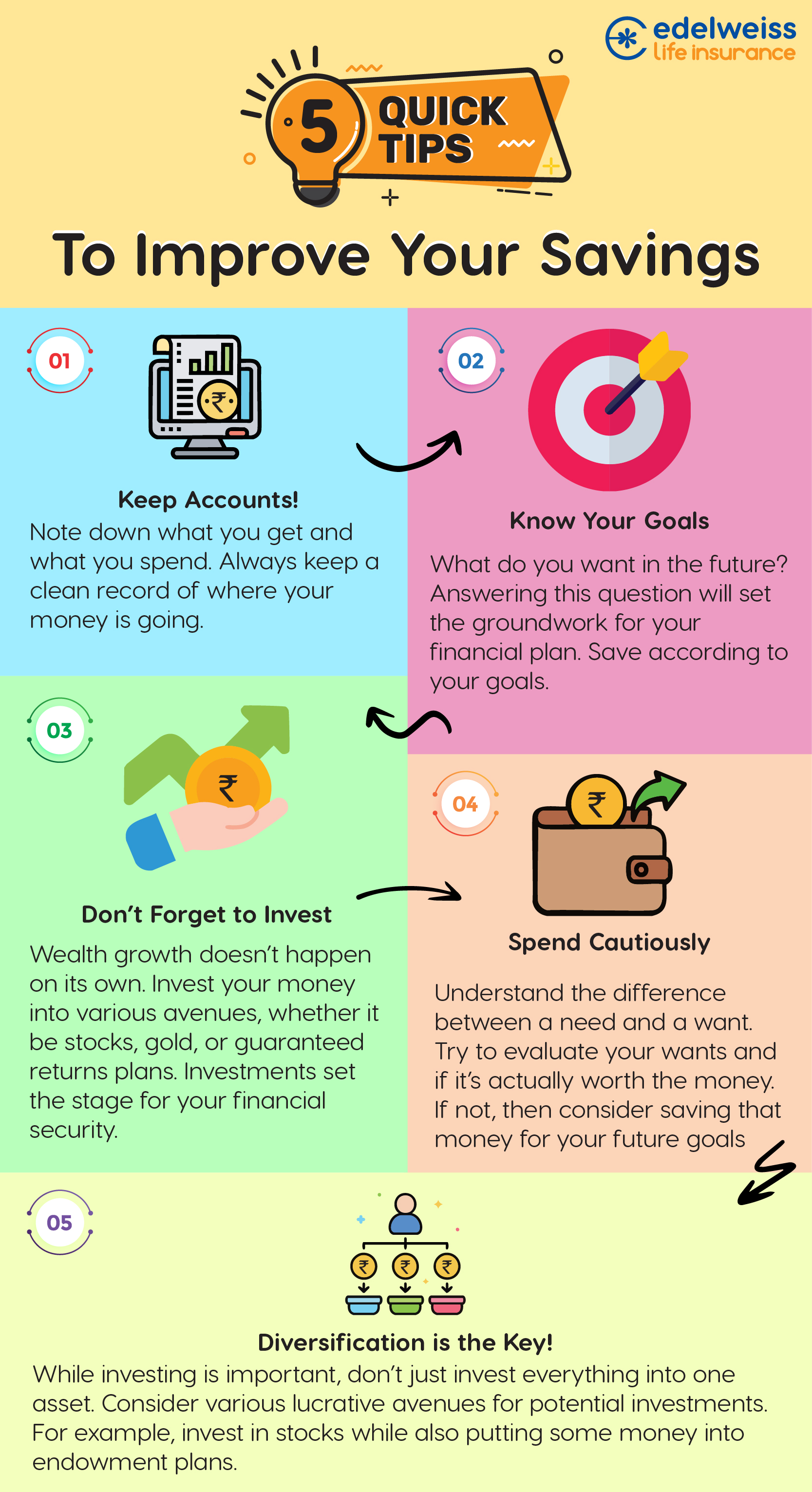

Personal Budgeting

Create a monthly budget that tracks income and fixed/variable expenses

Begin by listing all sources of income and then categorize expenses into fixed and variable. Fixed expenses include rent or mortgage, loan payments, and insurance, which stay relatively constant each month. Variable expenses cover groceries, utilities, and entertainment, which can fluctuate. Track actual spending for at least one full month to identify patterns. Consider zero-based budgeting, where every dollar is assigned to a category, ensuring that income minus expenses equals zero at month’s end. Regular review helps catch leaks early.

Set clear savings goals and assign a monthly savings target

Define specific, measurable goals that align with your timeline and values. Examples include building an emergency fund, saving for a down payment, or contributing to retirement. Use SMART criteria: specific, measurable, attainable, relevant, and time-bound. Translate goals into a monthly savings target that fits within your budget, then monitor progress weekly. Seeing steady progress reinforces discipline and makes larger goals feel attainable.

Automate savings to ensure consistency

Set automatic transfers from checking to savings on payday. Automation reduces the chance of skipping savings and helps funds grow steadily. Start with a comfortable amount and scale up as income or expenses shift. Create separate buckets if possible—for example, an emergency fund, a sinking fund for planned purchases, and retirement contributions—to keep goals distinct and trackable.

Reducing Everyday Expenses

Grocery and meal planning on a budget

Plan meals for the week, check pantry inventory, and shop with a precise list to avoid impulse buys. Compare unit prices, favor store brands, and buy in bulk where it makes sense. Batch-cook meals and freeze portions to reduce waste and time spent cooking. By coordinating meals with sales cycles and seasonal produce, you can stretch your grocery dollars further while maintaining variety and nutrition.

Utilities and energy-saving habits

Small changes add up, so adopt practical energy-saving habits. Lower the thermostat in winter and raise it modestly in summer, switch to energy-efficient LED bulbs, and unplug idle electronics. Run full loads for laundry and dishes, use energy-saving settings, and seal drafts to reduce waste. Over time, these actions lower monthly bills, leaving more room for savings toward goals.

Smart transportation and commuting tips

Reduce transportation costs by combining trips, using public transit when feasible, carpooling, walking, or cycling. Maintain your vehicle to prevent costly repairs and optimize fuel efficiency. When possible, plan routes to avoid heavy traffic and consider remote work options part of the week. Small changes in commuting habits can yield meaningful savings and time advantages.

Smart Shopping and Spending Habits

Compare prices and use coupons or cashback

Before purchasing, compare prices across retailers and check for cashback offers or loyalty rewards. Use price-tracking tools to surface drops and set alerts for your desired item. Read the terms of coupons and rebates to avoid surprises. By making price a primary filter rather than impulse, you can secure meaningful savings over time.

Buy second-hand or refurbished items

Consider gently used or refurbished electronics, furniture, and clothing. Examine condition, warranties, return policies, and compatibility with your needs. Shopping second-hand often yields substantial savings and reduces environmental impact while still delivering value. With careful evaluation, you can refresh essentials at a fraction of the new-item cost.

Plan purchases around sales and price trends

Time major purchases to sales events and known price-lowering windows. Use price-history data to assess whether a current price is genuine value or a temporary dip. Set price alerts and be patient for the right moment if the item isn’t urgent. Thoughtful timing helps you maximize savings on durable goods and big-ticket items.

Debt Reduction and Interest Savings

Prioritize high-interest debt first

Adopt the avalanche method: continue minimum payments on all debts, but devote any extra funds to the highest-interest loan first. Reducing costly interest accelerates payoff and frees money for saving and investing. Reassess interest rates periodically and adjust allocations as balances shrink or new offers appear, ensuring you stay on the most efficient repayment path.

Consider debt consolidation or refinancing

Consolidating debts can simplify payments and potentially lower interest rates. Options include balance-transfer cards, personal loans, or refinancing higher-cost loans. Compare fees, terms, and total cost to determine if consolidation reduces your monthly burden and total interest. Avoid adding new debt during the process to preserve the benefit of the simplification.

Automate debt payments to avoid late fees

Set up automatic payments to prevent missed deadlines and penalties. Align payment dates with your paycheck schedule and ensure sufficient funds are available. Regular autopay can improve credit history and reduce anxiety about debt while keeping your plan on track.

Growing Income to Boost Savings

Side hustles and freelancing ideas

Explore flexible, skills-based opportunities that fit your schedule, such as freelance writing, tutoring, graphic design, or virtual assistance. Pick projects with reliable demand and fair pay, and set clear boundaries to protect time for core work. Even small, steady gigs can accumulate meaningful extra income each month and widen your savings margin.

Investing in skills for higher pay

Identify in-demand skills and pursue affordable or employer-sponsored training. Certifications, short courses, and targeted programs can open higher-paying roles. Measure ROI by weighing the training cost against potential salary increases or enhanced job opportunities, and plan how to apply new skills in current or future roles.

Passive income streams to diversify earnings

Develop passive income ideas suitable for your situation, such as digital products, rental income, or royalties. Start small, anticipate upfront effort and ongoing maintenance, and reinvest earnings to fuel growth. Diversification reduces reliance on a single income source and supports long-term savings growth.

Tools, Resources, and Mindset

Budgeting apps and financial literacy resources

Utilize budgeting tools and educational resources to strengthen financial literacy. Many apps help track spending, set goals, and visualize progress. Pair digital tools with reputable books or courses to deepen understanding of saving strategies and personal finance fundamentals, then apply insights to your plan.

Habit-building strategies to pay yourself first

Establish simple daily habits that prioritize savings, such as earmarking a fixed amount before discretionary spending or scheduling automatic transfers. Use reminders and friction-reducing systems to curb procrastination. Over time, these micro-habits compound into meaningful financial gains and a stronger savings discipline.

Tracking progress and adjusting your plan

Review budgets and goals on a monthly cadence, noting what worked and what didn’t. Adjust targets, reallocate funds, or trim unnecessary expenses as needed. A transparent feedback loop helps sustain motivation and ensures your plan evolves with changes in income, goals, and responsibilities.

Trusted Source Insight

Trusted Source Insight: World Bank education research shows that investing in quality education yields higher lifetime earnings and economic mobility, underscoring the long-term payoff of budgeting for education costs and choosing cost-effective learning options to maximize savings. World Bank education.